Interest Rate Politics

July 1, 2017

During the second quarter of 2017, equity markets outside of North America posted the strongest returns. The U.S. equity market provided a muted positive performance while Canadian equities finished the quarter in negative territory.

In Canada, equities, as represented by the S&P/TSX Composite Index (S&P/TSX), returned -1.6% over the quarter. Much like the first quarter of 2017, declining oil prices weighed heavily on the market as oil prices declined 9% during the second quarter and 14% on a year to date basis (the Energy sector represents one-fifth of the Canadian equity index). The Materials and Financials sectors also experienced negative performance while Healthcare and Industrials were the top performing sectors.

The S&P 500 Index in the United States, representing U.S. equities, returned 3.1% in local (USD) currency terms over the quarter which translated into a 0.7% return in Canadian dollar terms (the USD declined relative to the CAD). Similar to Canada, the Energy sector had a negative impact on the index’s performance while Healthcare was the strongest performing sector.

The MSCI EAFE Index, representing International Equities (Europe, Australasia, Far East), returned 3.9% in Canadian dollar terms over the quarter. Of the 11 sectors represented in the index, Energy was the only sector to experience declining returns over the quarter. The strongest performing sectors included Information Technology and Consumer Staples. Solid economic growth, as well as reduced political volatility were the main drivers behind strong performance. In the U.K., Prime Minister Teresa May’s decision to hold a snap election backfired, as the Conservative Party lost its majority position in parliament and was forced to form a coalition with the Northern Ireland Democratic Unionist Party. In France’s presidential election, Emmanuel Macron secured a parliamentary majority and defeated populist Marie Le Pen (a strong supporter of a “Frexit”).

Valuation levels in equity markets continue to remain high as price to earnings ratios for the S&P/TSX, S&P 500 and the MSCI EAFE are currently above their 10-year averages. These valuation levels remain vulnerable to any earnings growth or economic growth disappointments.

For the second time in 2017, the U.S. Federal Reserve raised interest rates by 0.25% on June 14, 2017, a move that was widely anticipated. In Canada, interest rate expectations changed significantly towards the end of the second quarter in reaction to hawkish comments by Bank of Canada Senior Deputy Governor Wilkins and Bank of Canada Governor Poloz, suggesting that the bank was moving closer to its first interest rate increase in almost seven years. The widely telegraphed interest rate increase did become a reality on July 12, 2017 when the Bank of Canada raised interest rates 0.25%.

Interest Rate Politics

Once again, political events were plentiful in the U.S. thanks to the Trump administration. Based on the first 185 days that President Trump has been in office, he may be the most unpredictable president the U.S. has encountered. This past quarter President Trump refused to commit the U.S. to the Paris Climate Change Accord much to the dismay of many, shared highly classified information with Russian officials and fired FBI Director James Comey, to name a few events.

President Trump has also been unsuccessful at moving his agenda forward. After more than one attempt, the Trump administration was unable to get senate approval for healthcare reforms.

This environment makes it challenging for market participants to forecast the magnitude and direction of the U.S. economy. Renegotiations regarding the North American Free Trade Agreement (NAFTA) are scheduled to begin in late August. Earlier this year, President Trump had gone back and forth with regards to the degree of changes for NAFTA, even suggesting that the U.S. may exit the agreement entirely. Most recently, the Trump administration appears to be softening its stance on the materiality of the changes and is currently developing its list of negotiating objectives. The final outcome of this renegotiation may or may not have impactful implications for the U.S., Canadian and Mexican economies.

Given the current political landscape, equity valuation levels may be vulnerable to a pull-back from the “Trump Rally”. Also, market consensus appears to be waning with regards to the magnitude for further interest rate increases as many are re-evaluating the ability of President Trump to get his proposed progrowth policies enacted. As a result, longer term interest rates declined in the U.S. in the latter part of this past quarter, resulting in a slight flattening of the yield curve.

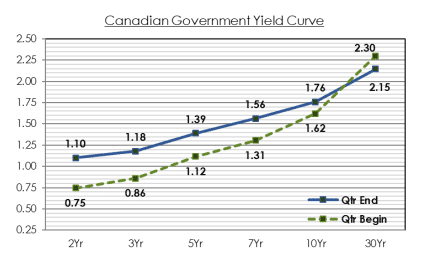

In Canada, the politics of the Bank of Canada took the spotlight with the rapid change in which interest rate expectations changed. Prior to signalling comments made by Bank of Canada officials, less than 5% of market participants expected an interest rate increase at the July 12, 2017 meeting (based on interest rate forward information). By the end of June this percentage had increased to almost 50% and by early July had surpassed 80%. This was triggered by public comments by Bank of Canada officials such as “we will be assessing whether all of the considerable monetary policy stimulus presently in place is still required” (Wilkins) and Governor Poloz that the two 2015 rate cuts have done their job and Canada now has “a much more diverse kind of recovery”.

In reaction, the Canadian yield curve underwent a noticeable transformation during the second quarter and flattened with short and mid-term interest rates rising and long-term interest rates declining slightly.

In terms of economic data to back the recent interest rate increase, the results are mixed. In support of higher interest rates is strong household spending, rising employment levels supported by 2.3% wage growth (was 1.2% for 2016), and real GDP growth expectations of 2.8%. On the other hand, inflation numbers have been soft, housing sales have started to decline (risking a housing correction) and household debt levels as a percentage of disposable income remain high, leaving us to wonder about the impact of increasing interest rates on this measure. In their July 12, 2017 Monetary Policy Report, the Bank of Canada did acknowledge the soft inflation data, calling it temporary due to electricity rebates in Ontario, changes in automobile pricing and heightened food price competition.

As the economic data did not have overall strong convictions, interest rates did not begin to increase until the Bank of Canada began making remarks regarding the potential for higher interest rates. In fact, interest rates in Canada were trending lower for the first part of the quarter leading to higher bond prices, which is why fixed income indices had a positive quarterly return overall (1.10% for the Canada Universe Bond Index).

In both Canada and the U.S., we saw politics at play for different reasons but both had their impact on interest rate expectations. In Canada, we were reminded how quickly expectations can be changed with a few simple, well placed comments by individuals in positions of authority (much like a political arena). In a further evaluation of these comments, the primary focus has been on the need to unwind the interest rate cuts that were put in place to deal with the aftermath of the 2008 financial crisis and not about inflationary concerns. The current low interest rate environment has been around much longer than anyone anticipated and there now appears to be a growing need by central banks to scale back this stimulus as supported by comments from other central banks. Bank of England Governor Mark Carney and European Central Bank head Mario Draghi have both hinted at interest rate increases in recent news. In a recent interview, former Bank of Canada Governor David Dodge recently commented that:

central banks should set aside inflation targeting temporarily and commit to gradually lifting interest rates from their current extreme lows to something approaching “normal” levels. There are more questions being raised as to whether targeting domestic inflation is as appropriate as it was 20 years ago. I don’t think any central bank really has a definitive answer to that. We’re all a little bit puzzled, quite frankly.

In other words, the decision to raise interest rates may be embarking on new territory and is currently not a simple response to an inflation rate target percentage. Instead, the decision is more subjective, making market participants more dependent on Bank of Canada officials for signals.

Given the strengthening expectations of interest rate increases (hence lower prices for fixed income products), we continue to keep fixed income portfolios positioned defensively to increasing interest rates while providing greater risk/reward metrics versus the broad fixed income market.

These times also serve as a reminder that portfolios should be positioned for the long term and not be influenced by short-term volatility. It doesn’t sound terribly exciting or glamorous but it works. To quote one of the foremost academic economists of the 20th century, Paul Samuelson, (Nobel Prize winner in economic sciences), “Investing should be more like watching paint dry or watching grass grow. If you want excitement, take $800 and go to Las Vegas”. Investing requires time and patience, regardless of how the politics may be playing out day-to-day.

When it comes to investing it is best to focus on things that you have control over. QAM maintains a long term view and focuses its efforts on asset allocation policy, manager selection, and systematic rebalancing in light of each client’s individual financial circumstances.

Disclaimer

This report may not be redistributed, retransmitted or disclosed, in whole or in part, or in any form or manner, without the express written consent of Quadrant Private Wealth ("Quadrant"). Any unauthorized use or disclosure is prohibited. The information herein was obtained from various sources believed to be reliable but Quadrant does not guarantee its accuracy. Neither Quadrant nor any director, officer or employee of Quadrant accepts any liability whatsoever for any direct, indirect or consequential damages or losses arising from any use of this report or its content. The opinions, estimates and projections contained in this report are as of the date indicated and are subject to change without notice. Certain of the statements may contain forward-looking statements which involve known and unknown risk, uncertainties and other factors which may cause the results, performance or achievements of the company, or industry results, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Past performance is not indicative of future performance. The content of this report is intended for information purposes only and does not constitute an offer to buy or sell our products or services.