2025 – Reflections on Uncertainty

October 14, 2025

As we enter the final quarter of 2025, it is a good time to provide a recap of the year so far and reflect on the current environment. The spheres of politics, economics, and financial markets have all experienced abrupt changes, and the general level of uncertainty has risen considerably. In times like these that are full of unknowns, it is important to focus on what is known and in your control.

2025 Recap

Politics

President Trump was inaugurated in January to serve his second term in office. The new administration immediately began issuing a flurry of executive orders for policies ranging from immigration enforcement to the renaming of the Gulf of Mexico. In the first 100 days of his presidency, Trump signed more executive orders than any other president in history (by a wide margin) over the same time frame.

Arguably the most impactful executive orders relate to the litany of tariffs that have been introduced during 2025. Typically under the purview of the U.S. Congress, Trump has exerted authority under controversial emergency or national security justifications in order to impose tariffs on a unilateral basis. It remains to be seen whether the U.S. Supreme Court will validate the tariffs or deem them illegal due to overreach of executive power. In the meantime, countries around the world have attempted to navigate the situation, with many negotiating new bilateral trade arrangements (favourable to the U.S.) to limit damage to their economies.

In Canada, Parliament was not in session for most of the year as the Liberal party found a new leader and called an election. Against the backdrop of a rapidly shifting U.S. relationship, former central banker Mark Carney was elected Prime Minister, leading the Liberals to a minority win and a fourth consecutive mandate. Carney is working to navigate the changing trade relationship with the U.S. and reinvigorate the Canadian economy, although it is too early to determine success on either front. Uncertainty will likely linger as the Canada-United States-Mexico Agreement (CUSMA) enters a renegotiation phase expected to extend well into 2026.

Economy

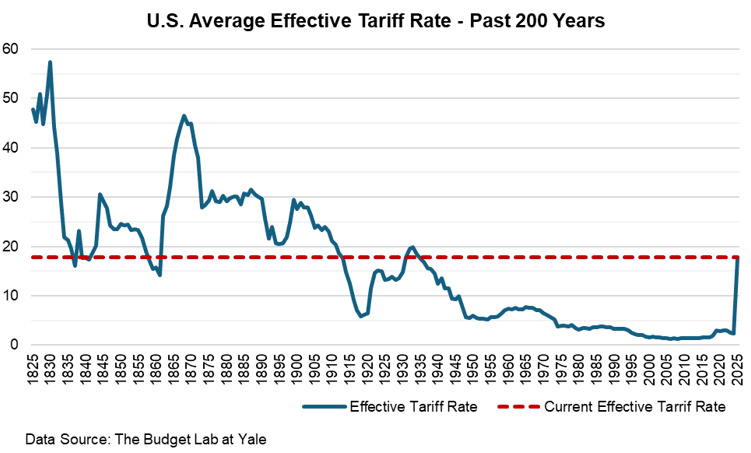

The imposition and threat of imposition of tariffs have been a dominant force impacting the global economy in 2025. The average U.S. tariff rate rose from approximately 2.4% to 28% following the “Liberation Day” announcements in April but has since declined to around 18% following a series of tariff delays and adjustments (too many to count). While down from the April peak, this marks the highest average U.S. tariff rate since 1934.

The ultimate impact of the new tariff regime remains uncertain. The U.S. economy has remained resilient so far, avoiding initial expectations of high inflation and slowed growth. However, due to numerous delays to tariff implementation and the lagged effect on the economy, it is too early to see the full impact. A full-blown global trade war has also been avoided for the time being, with most countries exercising patience and withholding from retaliatory tariffs.

The Canadian economy has fared relatively worse than the U.S. given approximately 75% of exports are sent to America. Canadian industries exposed to U.S. sectoral tariffs such as steel and aluminum, autos, lumber, and copper have been the most impacted, in addition to the canola and seafood industries that have been hit with separate Chinese tariffs. Despite these various sector-specific tariffs, the majority of Canadian trade with the U.S. continues to be shielded by the tariff-free CUSMA trade pact. After experiencing an economic contraction in the second quarter, growth has rebounded to an extent in the third quarter and economists now expect Canada to avoid the technical definition of recession – being two consecutive quarters of GDP contraction.

The Bank of Canada has reduced its policy interest rate three times so far this year, to a level of 2.50%. This compares to one interest rate reduction by the U.S. Federal Reserve in 2025 and a current target range of 4.00% to 4.25%. Relatively weaker growth, inflation near the central bank target, and a rise in unemployment levels has resulted in a faster pace of interest rate cuts in Canada compared to the U.S., which has seen resilient growth, above-target inflation, and low overall unemployment figures. Canada is expected to reduce its policy rate by 0.25% one more time by the end of the year while the U.S. is expected to cut once or twice more. Given the high level of uncertainty surrounding the tariff environment and the impacts on inflation and employment, these estimates can change rapidly.

Markets

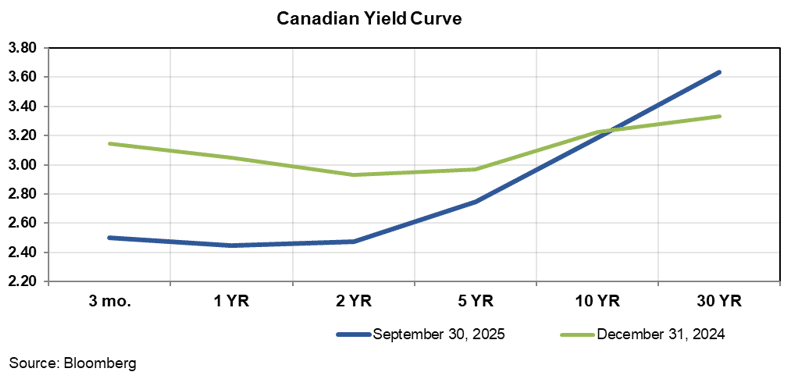

The broad Canadian fixed income market posted modest positive returns over the first three quarters of 2025, supported by central bank policy rate reductions noted above. The yield curve, a graphical representation of Canadian risk-free bond yields over increasing maturities, has steepened during the year as yields on shorter maturity bonds declined alongside the policy rate. Interestingly, yields on longer term bonds have either stayed steady or increased during this period, indicating expectations for higher long-term inflation or a higher risk premium demanded by investors for holding long maturity bonds.

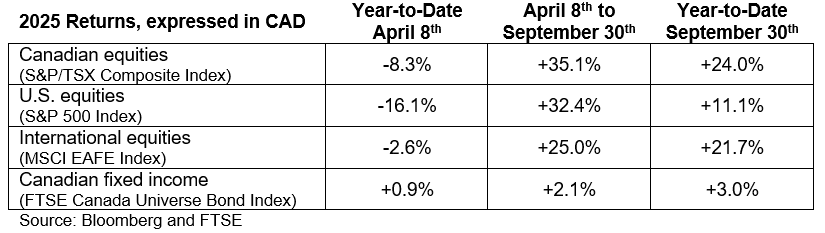

Global equity markets have been volatile in 2025. Broad equity markets experienced a notable sell-off in April following the U.S. tariff announcement shock, with the U.S. equity market seeing the largest declines. A week later, markets began to rebound as tariffs were delayed and it appeared that Trump’s announcements were more bark than bite. In the following months, despite a significantly higher U.S. tariff environment and economic uncertainty, equity markets looked past the turmoil and reached new all-time highs.

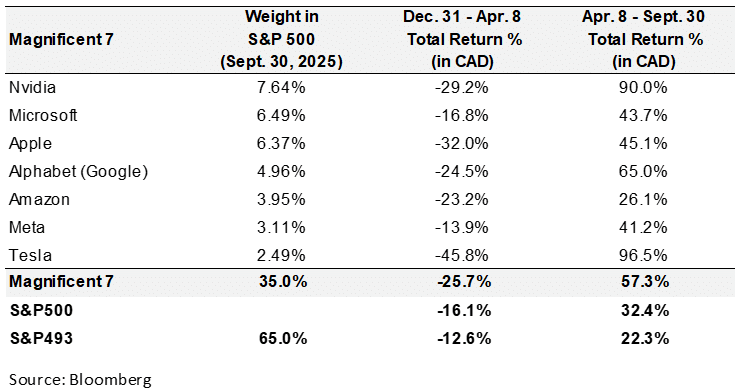

The “Magnificent 7” group of mega-cap technology related stocks has continued to have an outsized impact on U.S. equity market performance – for better or worse. During the market selloff earlier in the year, the Magnificent 7 declined more than the broad S&P 500 Index as their lofty valuations (average price-to-earnings ratio of approximately 33x at the time) left them with minimal margins of safety. The Magnificent 7 then experienced a rapid rebound following the market bottom in April, fueled in part by high expectations surrounding the artificial intelligence (AI) theme.

While earnings for the Magnificent 7 have been robust and growing on average, arguably elevated valuation levels and increasing concentration within the index represent risks for the S&P 500 as a whole. As of September 30th, the Magnificent 7 made up 35% of the entire S&P 500 Index (a historically high level of concentration) and have accounted for approximately 50% of the index return since April 8th.

The Canadian equity market has been a top performer in 2025 despite economic challenges in Canada – a good reminder that the stock market is not the economy. The materials sector was the largest contributor to performance, benefitting from a significant increase in the price of gold and other commodity prices. Energy and financials, the two largest sectors in the Canadian index, have also been notable contributors, supported by commodity prices and lower interest rates.

International equity market performance was driven by the three largest sectors – financials, industrials, and technology. The financials sector benefitted from easing monetary policy and resilient earnings while the technology sector benefitted from exposure to the AI theme. The industrials sector was supported by European defense related firms as Europe announced a major rearmament strategy against a backdrop of continued Russian aggression and declining reliability of U.S. security guarantees.

On the heels of double-digit returns so far during 2025, overall valuation levels across developed market equity indices have increased and are now elevated compared to long term averages. The U.S. equity market in particular continues to be the most expensive on a relative basis and is near historical extremes based on numerous metrics. Is this sustainable?

Unknowns and Knowns

Due to the nature of the financial markets, we know that uncertainty is a certainty even in the best of times. Given the current environment, it feels like there is more uncertainty than normal. Are current valuations sustainable? Will the Magnificent 7 continue to outperform? Is AI in a bubble? What will Trump do next? Will Canada enter a recession? Will tariffs reignite inflation? Where will interest rates be next year?

The list of questions can go on but the reality is that no one can know with certainty, the answers.

Here is what we do know:

- Stock market valuations can remain elevated or even continue to rise further for extended periods of time irrespective of economic uncertainty.

- A well constructed portfolio that is properly diversified across asset classes, geographies, and underlying securities will provide resiliency across different market environments.

- Paying attention to risk is paramount. At Quadrant, we partner with institutional asset class managers that have demonstrated a risk-focused approach to asset class management over various market cycles.

- Behavioural biases can get you into trouble. Fear of missing out (FOMO) and chasing recent returns is not a strategy.

- A rules-based approach to portfolio rebalancing ensures your portfolio maintains its desired risk exposures while removing emotion from the process.

- Markets are volatile and unpredictable in the short term. Dedication to a well-thought-out investment process over time is required for long term success and compounding of wealth.

In times that are full of unknowns, it is best to focus instead on what is known and in your control.

Download this newsletter as a PDF.

About Us

Disciplined. Compassionate. Effective.

Quadrant Private Wealth is an independent, comprehensive, integrated wealth management firm committed to your financial well-being and peace of mind. We take the time to understand your complete financial picture. We tie all of your information together, including tax planning, to paint a picture of what your financial future could look like. And we aim to earn your complete confidence in the process.

Quadrant Private Wealth

Suite 720, One Lombard Pl

Winnipeg, MB

Ph: (204) 944-8124

email: inquiries@quadrantprivate.com

web: www.quadrantprivate.com

Disclaimer

This report may not be redistributed, retransmitted or disclosed, in whole or in part, or in any form or manner, without the express written consent of Quadrant Private Wealth ("Quadrant"). Any unauthorized use or disclosure is prohibited. The information herein was obtained from various sources believed to be reliable but Quadrant does not guarantee its accuracy. Neither Quadrant nor any director, officer or employee of Quadrant accepts any liability whatsoever for any direct, indirect or consequential damages or losses arising from any use of this report or its content. The opinions, estimates and projections contained in this report are as of the date indicated and are subject to change without notice. Certain of the statements may contain forward-looking statements which involve known and unknown risk, uncertainties and other factors which may cause the results, performance or achievements of the company, or industry results, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Past performance is not indicative of future performance. The content of this report is intended for information purposes only and does not constitute an offer to buy or sell our products or services.